| [1] |

Pamela M, Dick C, Moerman L. Creating institutional meaning: Accounting and taxation law perspectives of carbon permits. Critical Perspectives on Accounting, 2010, 21 (07): 619–630. doi: 10.1016/j.cpa.2010.03.006

|

| [2] |

Convery F J, Redmond L. Market and price developments in the European Union Emissions Trading scheme. Review of Environmental Economics and Policy, 2007, 1 (01): 88–111. doi: 10.1093/reep/rem010

|

| [3] |

Cao G, Xu W. Nonlinear structure analysis of carbon and energy markets with MFDCCA based on maximum overlap wavelet transform. Physica A, 2015, 444 (2016): 505–523.

|

| [4] |

Kumar S, Managi S, Matsuda A. Stock prices of clean energy firms, oil and carbon markets: A vector autoregressive analysis. Energy Economics, 2012, 34 (01): 215–226. doi: 10.1016/j.eneco.2011.03.002

|

| [5] |

Uddin G S. Multivariate dependence and spillover effects across energy commodities and diversification potentials of carbon assets. Energy Economics, 2018, 78 (01): 215–226.

|

| [6] |

Guo W J. Factors impacting on the price of China’s regional carbon emissions based on adaptive Lasson method. China Population, Resources and Environment, 2015, 25 (01): 305–310.

|

| [7] |

Tao C H. A study on the dynamic correlation between carbon emission trade and the stock market of China. Journal of Beijing Jiaotong University, 2015, 14 (04): 40–51.

|

| [8] |

Zhu D S. A study on the relationship between stock prices of companies of low carbon economy & new energy and the price of carbon allowances. Ecological Economy, 2016, 32 (01): 52–57.

|

| [9] |

Cui J, Huang J, Li K. Research on the relationship between carbon emission spot prices, energy prices and the Dow Jones index of China based on VAR. On Economic Problems, 2018, 07: 27–33.

|

| [10] |

Wei Q, Jin Z R. Study on the impact of changes in fossil energy prices on China’s carbon trading prices. Price:Theory & Practice, 2018, 11: 42–45.

|

| [11] |

Zou S H, Zhang T. Dynamic analysis of nonlinear relations between energy futures, energy stocks and carbon markets. Systems Engineering, 2020, 38 (05): 1–13.

|

| [12] |

Liu J H, Liang J L, Chen X. Research on risk spillover effect of China’s carbon market, domestic coke market and EU EIS. Journal of Industrial Technological Economics, 2020, 09: 88–95.

|

| [13] |

Xu Y Y. Risk spillover from energy market uncertainties to the Chinese carbon market. Pacific-Basin Finance Journal, 2021, 67.

|

| [14] |

Wang X, Qiao Q W, Chen X. Study on the dynamic dependence between carbon emission trading market and new energy market: A case study of China's carbon market pilot. Journal of China University of Mining and Technology (Social Sciences), 2021, 23 (06): 89–106.

|

| [15] |

Zhao L D, Fan C, Wang H X. The time-varying spillover effects between China’s carbon markets and energy market —An empirical study based on spillover index model. Journal of Beijing institute of Technology (Social Sciences Edition), 2021, 23 (01): 28–40.

|

| [16] |

Zhang S B, Ji H, Tian M X, et al. High-dimensional nonlinear dependence and risk spillovers analysis between China’s carbon market and its major influence factors. Annals of Operations Research, 2022, 06: 1–30.

|

| [17] |

Yao Y, Tian G X, Cao G X. Information spillover among the carbon market, energy market, and stock market: A case study of China’s pilot carbon markets. Sustainability, 2022, 14 (08): 44–79.

|

| [18] |

Wang X P, Wang W C. The risk spillover effect between carbon market and stock markets. Journal of Technology Economics, 2022, 41 (06): 131–142.

|

| [19] |

Chen X H, Wang Z J. Empirical research on rice impact factor of carbon emission exchange: Evidence from EU ETS. Systems Engineering, 2012, 30 (02): 53–60.

|

| [20] |

Hrischman A O. The Strategy of Economic Development. New Haven: Yale University Press, 1998, 16.

|

| [21] |

Lv J Y, Fan X Y, Wu H N. Sensitivity analysis of factors influencing carbon prices in China. Soft Science, 2021, 35 (05): 123–130.

|

| [22] |

Wang K M. Modelling the nonlinear relationship between CO2 emissions from oil and economic growth. Econnomic Modelling, 2012, 29 (05): 1537–1547. doi: 10.1016/j.econmod.2012.05.001

|

| [23] |

Diebold F X, Yilmaz K. Measuring financial asset return and volatility spillovers with application to global equity markets. Economic Journal, 2009, 119: 158–171. doi: 10.1111/j.1468-0297.2008.02208.x

|

| [24] |

Diebold F X, Yilmaz K. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting, 2012, 28: 57–66. doi: 10.1016/j.ijforecast.2011.02.006

|

| [25] |

Diebold F X, Yilmaz K. On the network topology of variance decompositions: measuring the connectedness of financial firms. Journal of Econometrics, 2014, 182 (1): 119–134. doi: 10.1016/j.jeconom.2014.04.012

|

| [26] |

Antonakakis N, Chatziantoniou I, Gabauer D. Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions. Journal of Risk and Financial Management, 2020, 13 (04): 84–107. doi: 10.3390/jrfm13040084

|

| [27] |

Koop G, Korobilis D. Large time-varying parameter VARs. Journal of Econometrics, 2013, 177: 158–198.

|

| [28] |

Adekoya O B, Akinseye A B, Antonakakis N and, et al. Crude oil and Islamic sectoral stocks: Asymmetric TVP-VAR connectedness and investment strategies. Resources Policy, 2022, 78: 102877. doi: 10.1016/j.resourpol.2022.102877

|

| [29] |

Gabauer D. Dynamic measures of asymmetric & pairwise connectedness within an optimal currency area: Evidence from the ERM I system. Journal of Multinational Financial Management, 2021, 60: 100680. doi: 10.1016/j.mulfin.2021.100680

|

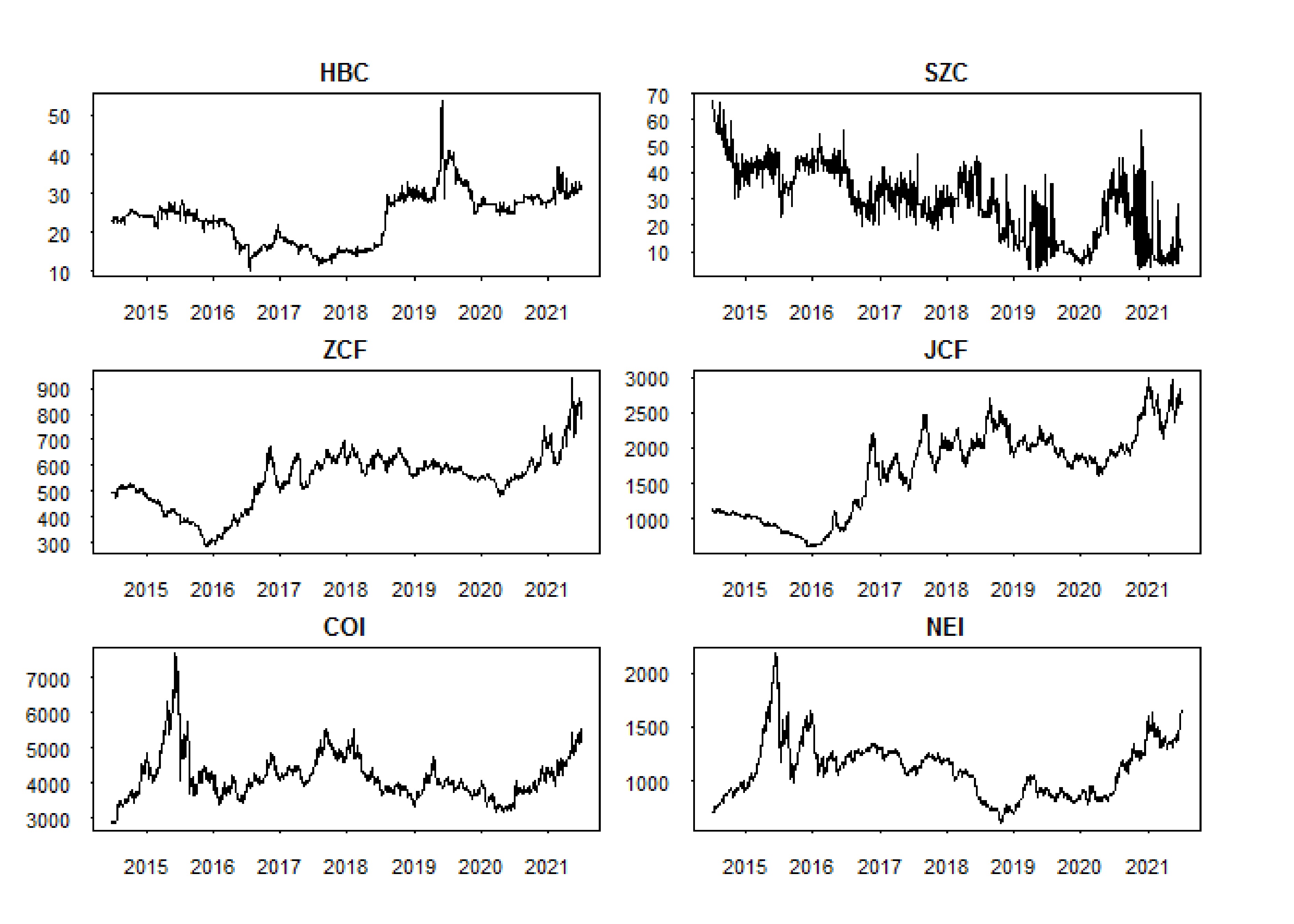

Figure 1. Closing prices of each market

Figure 2. Dynamic total connectedness

Figure 3. Dynamic net total directional connectedness

Figure 4. Dynamic net pairwise directional connectedness

Figure 5. Dynamic pairwise connectedness

| [1] |

Pamela M, Dick C, Moerman L. Creating institutional meaning: Accounting and taxation law perspectives of carbon permits. Critical Perspectives on Accounting, 2010, 21 (07): 619–630. doi: 10.1016/j.cpa.2010.03.006

|

| [2] |

Convery F J, Redmond L. Market and price developments in the European Union Emissions Trading scheme. Review of Environmental Economics and Policy, 2007, 1 (01): 88–111. doi: 10.1093/reep/rem010

|

| [3] |

Cao G, Xu W. Nonlinear structure analysis of carbon and energy markets with MFDCCA based on maximum overlap wavelet transform. Physica A, 2015, 444 (2016): 505–523.

|

| [4] |

Kumar S, Managi S, Matsuda A. Stock prices of clean energy firms, oil and carbon markets: A vector autoregressive analysis. Energy Economics, 2012, 34 (01): 215–226. doi: 10.1016/j.eneco.2011.03.002

|

| [5] |

Uddin G S. Multivariate dependence and spillover effects across energy commodities and diversification potentials of carbon assets. Energy Economics, 2018, 78 (01): 215–226.

|

| [6] |

Guo W J. Factors impacting on the price of China’s regional carbon emissions based on adaptive Lasson method. China Population, Resources and Environment, 2015, 25 (01): 305–310.

|

| [7] |

Tao C H. A study on the dynamic correlation between carbon emission trade and the stock market of China. Journal of Beijing Jiaotong University, 2015, 14 (04): 40–51.

|

| [8] |

Zhu D S. A study on the relationship between stock prices of companies of low carbon economy & new energy and the price of carbon allowances. Ecological Economy, 2016, 32 (01): 52–57.

|

| [9] |

Cui J, Huang J, Li K. Research on the relationship between carbon emission spot prices, energy prices and the Dow Jones index of China based on VAR. On Economic Problems, 2018, 07: 27–33.

|

| [10] |

Wei Q, Jin Z R. Study on the impact of changes in fossil energy prices on China’s carbon trading prices. Price:Theory & Practice, 2018, 11: 42–45.

|

| [11] |

Zou S H, Zhang T. Dynamic analysis of nonlinear relations between energy futures, energy stocks and carbon markets. Systems Engineering, 2020, 38 (05): 1–13.

|

| [12] |

Liu J H, Liang J L, Chen X. Research on risk spillover effect of China’s carbon market, domestic coke market and EU EIS. Journal of Industrial Technological Economics, 2020, 09: 88–95.

|

| [13] |

Xu Y Y. Risk spillover from energy market uncertainties to the Chinese carbon market. Pacific-Basin Finance Journal, 2021, 67.

|

| [14] |

Wang X, Qiao Q W, Chen X. Study on the dynamic dependence between carbon emission trading market and new energy market: A case study of China's carbon market pilot. Journal of China University of Mining and Technology (Social Sciences), 2021, 23 (06): 89–106.

|

| [15] |

Zhao L D, Fan C, Wang H X. The time-varying spillover effects between China’s carbon markets and energy market —An empirical study based on spillover index model. Journal of Beijing institute of Technology (Social Sciences Edition), 2021, 23 (01): 28–40.

|

| [16] |

Zhang S B, Ji H, Tian M X, et al. High-dimensional nonlinear dependence and risk spillovers analysis between China’s carbon market and its major influence factors. Annals of Operations Research, 2022, 06: 1–30.

|

| [17] |

Yao Y, Tian G X, Cao G X. Information spillover among the carbon market, energy market, and stock market: A case study of China’s pilot carbon markets. Sustainability, 2022, 14 (08): 44–79.

|

| [18] |

Wang X P, Wang W C. The risk spillover effect between carbon market and stock markets. Journal of Technology Economics, 2022, 41 (06): 131–142.

|

| [19] |

Chen X H, Wang Z J. Empirical research on rice impact factor of carbon emission exchange: Evidence from EU ETS. Systems Engineering, 2012, 30 (02): 53–60.

|

| [20] |

Hrischman A O. The Strategy of Economic Development. New Haven: Yale University Press, 1998, 16.

|

| [21] |

Lv J Y, Fan X Y, Wu H N. Sensitivity analysis of factors influencing carbon prices in China. Soft Science, 2021, 35 (05): 123–130.

|

| [22] |

Wang K M. Modelling the nonlinear relationship between CO2 emissions from oil and economic growth. Econnomic Modelling, 2012, 29 (05): 1537–1547. doi: 10.1016/j.econmod.2012.05.001

|

| [23] |

Diebold F X, Yilmaz K. Measuring financial asset return and volatility spillovers with application to global equity markets. Economic Journal, 2009, 119: 158–171. doi: 10.1111/j.1468-0297.2008.02208.x

|

| [24] |

Diebold F X, Yilmaz K. Better to give than to receive: Predictive directional measurement of volatility spillovers. International Journal of Forecasting, 2012, 28: 57–66. doi: 10.1016/j.ijforecast.2011.02.006

|

| [25] |

Diebold F X, Yilmaz K. On the network topology of variance decompositions: measuring the connectedness of financial firms. Journal of Econometrics, 2014, 182 (1): 119–134. doi: 10.1016/j.jeconom.2014.04.012

|

| [26] |

Antonakakis N, Chatziantoniou I, Gabauer D. Refined measures of dynamic connectedness based on time-varying parameter vector autoregressions. Journal of Risk and Financial Management, 2020, 13 (04): 84–107. doi: 10.3390/jrfm13040084

|

| [27] |

Koop G, Korobilis D. Large time-varying parameter VARs. Journal of Econometrics, 2013, 177: 158–198.

|

| [28] |

Adekoya O B, Akinseye A B, Antonakakis N and, et al. Crude oil and Islamic sectoral stocks: Asymmetric TVP-VAR connectedness and investment strategies. Resources Policy, 2022, 78: 102877. doi: 10.1016/j.resourpol.2022.102877

|

| [29] |

Gabauer D. Dynamic measures of asymmetric & pairwise connectedness within an optimal currency area: Evidence from the ERM I system. Journal of Multinational Financial Management, 2021, 60: 100680. doi: 10.1016/j.mulfin.2021.100680

|

ISSN 0253-2778

CN 34-1054/N

Copyright © Editorial Office of JUSTC, All Rights Reserved. 皖ICP备05002528号

Supported by:

Beijing Renhe Information Technology Co. Ltd

DownLoad:

DownLoad: